Page 40 - 5.2 i. Manac Costing ITC Summarised Notes

P. 40

ITC EXAM PREP

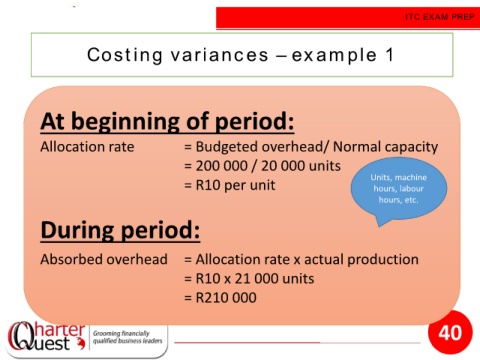

Costing variances – example 1

At beginning of period:

Allocation rate = Budgeted overhead/ Normal capacity

= 200 000 / 20 000 units

= R10 per unit Units, machine

hours, labour

hours, etc.

During period:

Absorbed overhead = Allocation rate x actual production

= R10 x 21 000 units

= R210 000

40