Page 155 - Capricorn IAR 2020

P. 155

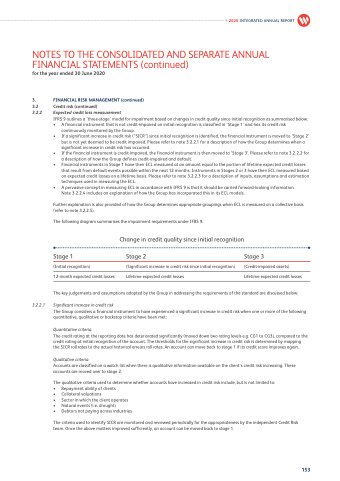

Change in credit quality since initial recognition

2020 INTEGRATED ANNUAL REPORT

NOTES TO THE CONSOLIDATED AND SEPARATE ANNUAL FINANCIAL STATEMENTS (continued)

for the year ended 30 June 2020

3. FINANCIAL RISK MANAGEMENT (continued)

3.2 Credit risk (continued)

3.2.2 Expected credit loss measurement

IFRS 9 outlines a ‘three-stage’ model for impairment based on changes in credit quality since initial recognition as summarised below:

• A financial instrument that is not credit-impaired on initial recognition is classified in ‘Stage 1’ and has its credit risk

continuously monitored by the Group.

• If a significant increase in credit risk (“SICR”) since initial recognition is identified, the financial instrument is moved to ‘Stage 2’

but is not yet deemed to be credit impaired. Please refer to note 3.2.2.1 for a description of how the Group determines when a

significant increase in credit risk has occurred.

• If the financial instrument is credit-impaired, the financial instrument is then moved to ‘Stage 3’. Please refer to note 3.2.2.2 for

a description of how the Group defines credit-impaired and default.

• Financial instruments in Stage 1 have their ECL measured at an amount equal to the portion of lifetime expected credit losses

that result from default events possible within the next 12 months. Instruments in Stages 2 or 3 have their ECL measured based on expected credit losses on a lifetime basis. Please refer to note 3.2.2.3 for a description of inputs, assumptions and estimation techniques used in measuring the ECL.

• A pervasive concept in measuring ECL in accordance with IFRS 9 is that it should be carried forward-looking information. Note 3.2.2.4 includes an explanation of how the Group has incorporated this in its ECL models.

Further explanation is also provided of how the Group determines appropriate groupings when ECL is measured on a collective basis (refer to note 3.2.2.5).

The following diagram summarises the impairment requirements under IFRS 9:

Stage 1

(Initial recognition)

12-month expected credit losses

Stage 2

(Significant increase in credit risk since initial recognition) Lifetime expected credit losses

Stage 3

(Credit-impaired assets) Lifetime expected credit losses

The key judgements and assumptions adopted by the Group in addressing the requirements of the standard are discussed below:

3.2.2.1 Significant increase in credit risk

The Group considers a financial instrument to have experienced a significant increase in credit risk when one or more of the following quantitative, qualitative or backstop criteria have been met:

Quantitative criteria

The credit rating at the reporting date has deteriorated significantly (moved down two rating levels e.g. CG1 to CG3), compared to the credit rating at initial recognition of the account. The thresholds for the significant increase in credit risk is determined by mapping the SICR roll rates to the actual historical arrears roll rates. An account can move back to stage 1 if its credit score improves again.

Qualitative criteria

Accounts are classified on a watch list when there is qualitative information available on the client’s credit risk increasing. These accounts are moved over to stage 2.

The qualitative criteria used to determine whether accounts have increased in credit risk include, but is not limited to:

• Repayment ability of clients

• Collateral valuations

• Sector in which the client operates

• Natural events (i.e. drought)

• Debtors not paying across industries

The criteria used to identify SICR are monitored and reviewed periodically for the appropriateness by the independent Credit Risk team. Once the above matters improved sufficiently, an account can be moved back to stage 1.

153