Page 5 - DMEA 32

P. 5

DMEA COMMENTARY DMEA

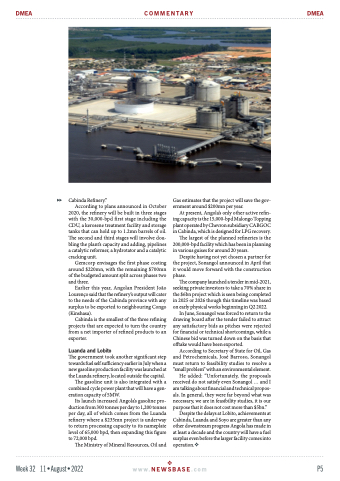

Cabinda Refinery.”

According to plans announced in October

2020, the refinery will be built in three stages with the 30,000-bpd first stage including the CDU, a kerosene treatment facility and storage tanks that can hold up to 1.2mn barrels of oil. The second and third stages will involve dou- bling the plant’s capacity and adding, pipelines a catalytic reformer, a hydrotator and a catalytic cracking unit.

Gemcorp envisages the first phase costing around $220mn, with the remaining $700mn of the budgeted amount split across phases two and three.

Earlier this year, Angolan President João Lourenço said that the refinery’s output will cater to the needs of the Cabinda province with any surplus to be exported to neighbouring Congo (Kinshasa).

Cabinda is the smallest of the three refining projects that are expected to turn the country from a net importer of refined products to an exporter.

Luanda and Lobito

The government took another significant step towards fuel self sufficiency earlier in July when a new gasoline production facility was launched at the Luanda refinery, located outside the capital.

The gasoline unit is also integrated with a combined cycle power plant that will have a gen- eration capacity of 5MW.

Its launch increased Angola’s gasoline pro- ductionfrom300tonnesperdayto1,200tonnes per day, all of which comes from the Luanda refinery where a $235mn project is underway to return processing capacity to its nameplate level of 65,000 bpd, then expanding this figure to 72,000 bpd.

The Ministry of Mineral Resources, Oil and

Gas estimates that the project will save the gov- ernment around $200mn per year.

At present, Angola’s only other active refin- ing capacity is the 15,000-bpd Malongo Topping plant operated by Chevron subsidiary CABGOC in Cabinda, which is designed for LPG recovery.

The largest of the planned refineries is the 200,000-bpd facility which has been in planning in various guises for around 20 years.

Despite having not yet chosen a partner for the project, Sonangol announced in April that it would move forward with the construction phase.

The company launched a tender in mid-2021, seeking private investors to take a 70% share in the $6bn project which is seen being completed in 2025 or 2026 though this timeline was based on early physical works beginning in Q2 2022.

In June, Sonangol was forced to return to the drawing board after the tender failed to attract any satisfactory bids as pitches were rejected for financial or technical shortcomings, while a Chinese bid was turned down on the basis that offtake would have been exported.

According to Secretary of State for Oil, Gas and Petrochemicals, José Barroso, Sonangol must return to feasibility studies to resolve a “small problem” with an environmental element.

He added: “Unfortunately, the proposals received do not satisfy even Sonangol ... and I am talking about financial and technical propos- als. In general, they were far beyond what was necessary, we are in feasibility studies, it is our purposethatitdoesnotcostmorethan$5bn.”

Despite the delays at Lobito, achievements at Cabinda, Luanda and Soyo are greater than any other downstream progress Angola has made in at least a decade and the country will have a fuel surplus even before the larger facility comes into operation.

Week 32 11•August•2022 w w w . N E W S B A S E . c o m P5