Page 23 - bne IntelliNews monthly magazine April 2025

P. 23

bne April 2025 Companies & Markets I 23

The EU must bet on nuclear

Owen Walden-Harris

The European Union’s commitment to reaching net zero greenhouse gas emissions, generating 75% of its electricity from renewables and mobilising €1 trillion in green finance investments by the 2050s is undeniably ambitious. Yet beneath this visionary agenda lies a critical flaw: the marginalisation of the nuclear sector.

While not excluded from the EU’s plans, the EU’s Sustainable Finance Framework and taxonomy make it difficult

and burdensome to finance nuclear projects. This risks suffocating the bloc's green ambitions before they can even take off. The difficulties that it has generated have created

a tendency towards an over reliance on renewable energy for the green transition. This over reliance could easily undermine the EU’s ability to meet its own climate goals and may well reduce its economic resilience in the future.

From a Central and Eastern European perspective, this will compound the already significant challenge of shifting from an outdated, predominantly coal and natural gas based energy network to a more modern mix of renewables and nuclear power. It will both reduce the scope of nuclear investments and create regulatory hurdles.

It would, however, be tabloid to claim that the EU’s taxonomy prevents its member states from pursuing nuclear projects. It is simply the case that it will over the long term make nuclear projects harder to finance and less numerous than those found in other major economies. The global norm is for a balanced mixture of renewables and nuclear as fossil fuels are gradually phased out. This makes the EU’s approach a uniquely European experiment. An experiment which if handled poorly could negatively affect the bloc’s economy for decades to come but no more so than in its Central and East European member states, which are further behind in the green transition.

Nominally, the EU’s Taxonomy Regulation (2020/852) includes nuclear energy as a sustainable investment option. In practice nuclear projects face additional regulatory hurdles that renew- able projects don't. The EU’s taxonomy has created a stringent criteria for such projects to pass in order to access funding with a strong emphasis on waste management and safety. It's understandable for the EU to want a strong emphasis on safety

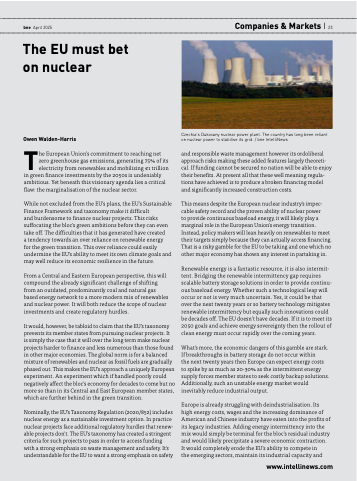

Czechia's Dukovany nuclear power plant. The country has long been reliant on nuclear power to stabilise its grid. / bne IntelliNews

and responsible waste management however its ordoliberal approach risks making these added features largely theoreti- cal. If funding cannot be secured no nation will be able to enjoy their benefits. At present all that these well meaning regula- tions have achieved is to produce a broken financing model and significantly increased construction costs.

This means despite the European nuclear industry's impec- cable safety record and the proven ability of nuclear power

to provide continuous baseload energy, it will likely play a marginal role in the European Union's energy transition. Instead, policy makers will lean heavily on renewables to meet their targets simply because they can actually access financing. That is a risky gamble for the EU to be taking and one which no other major economy has shown any interest in partaking in.

Renewable energy is a fantastic resource, it is also intermit- tent. Bridging the renewable intermittency gap requires scalable battery storage solutions in order to provide continu- ous baseload energy. Whether such a technological leap will occur or not is very much uncertain. Yes, it could be that over the next twenty years or so battery technology mitigates renewable intermittency but equally such innovations could be decades off. The EU doesn’t have decades. If it is to meet its 2050 goals and achieve energy sovereignty then the rollout of clean energy must occur rapidly over the coming years.

What's more, the economic dangers of this gamble are stark. If breakthroughs in battery storage do not occur within

the next twenty years then Europe can expect energy costs to spike by as much as 20-30% as the intermittent energy supply forces member states to seek costly backup solutions. Additionally, such an unstable energy market would inevitably reduce industrial output.

Europe is already struggling with deindustrialisation. Its high energy costs, wages and the increasing dominance of American and Chinese industry have eaten into the profits of its legacy industries. Adding energy intermittency into the mix would simply be terminal for the bloc’s residual industry and would likely precipitate a severe economic contraction. It would completely erode the EU’s ability to compete in

the emerging sectors, maintain its industrial capacity and

www.intellinews.com