Page 135 - Policy Wording - Hollard Business Binder (2020-08-26)

P. 135

Motor Traders

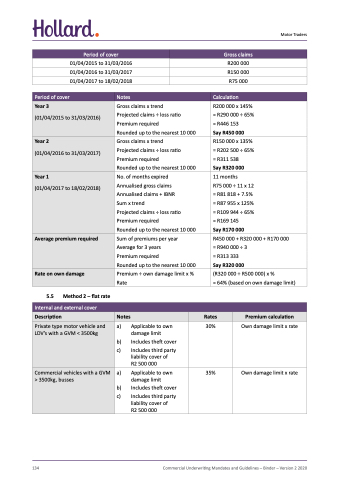

Period of cover

R200 000 R150 000 R75 000

R200 000 x 145% = R290 000 ÷ 65% = R446 153

Say R450 000 R150 000 x 135% = R202 500 ÷ 65% = R311 538

Say R320 000

11 months

R75 000 ÷ 11 x 12

= R81 818 + 7.5%

= R87 955 x 125%

= R109 944 ÷ 65%

= R169 145

Say R170 000

R450 000 + R320 000 + R170 000

= R940 000 ÷ 3

= R313 333

Say R320 000

(R320 000 ÷ R500 000) x %

= 64% (based on own damage limit)

Period of cover

Year 2

(01/04/2016 to 31/03/2017)

Notes

Projected claims ÷ loss ratio

Premium required

Rounded up to the nearest 10 000

Calculation

Year 3

(01/04/2015 to 31/03/2016)

Gross claims x trend

Gross claims x trend

Projected claims ÷ loss ratio

Premium required

Rounded up to the nearest 10 000

Year 1

(01/04/2017 to 18/02/2018)

No. of months expired

Annualised gross claims

Annualised claims + IBNR

Sum x trend

Projected claims ÷ loss ratio

Premium required

Rounded up to the nearest 10 000

Average premium required

Sum of premiums per year

Average for 3 years

Premium required

Rounded up to the nearest 10 000

Rate on own damage

Premium ÷ own damage limit x %

Rate

5.5

Method 2 – flat rate

Internal and external cover

Description

Notes

Rates

Premium calculation

Private type motor vehicle and LDV’s with a GVM < 3500kg

a) Applicable to own damage limit

b) Includes theft cover

c) Includes third party liability cover of

R2 500 000

30%

Own damage limit x rate

Commercial vehicles with a GVM > 3500kg, busses

a) Applicable to own damage limit

b) Includes theft cover

c) Includes third party liability cover of

R2 500 000

35%

Own damage limit x rate

134

Commercial Underwriting Mandates and Guidelines – Binder – Version 2 2020

Gross claims

01/04/2015 to 31/03/2016

01/04/2016 to 31/03/2017

01/04/2017 to 18/02/2018