Page 16 - November 2020 WCA Ketch Pen

P. 16

16

Cull Cow Market Review and Outlook

By: Shannon Neibergs, Professor/Extension Economist at Washington State University

Given the Covid-19 pandemic effects on cattle markets

it is interesting to evaluate impacts and outlook on the

cull cow market considering the economic factors at work. Within the seasonal cow slaughter pattern, it is essential to look for non-typical changes to evaluate market conditions. For beef cows, large changes in slaughter numbers are usually associated with drought risk. The drought from 2011 to 2014 throughout the Southern Plains was a leading cause of large cow inventory liquidations that supported

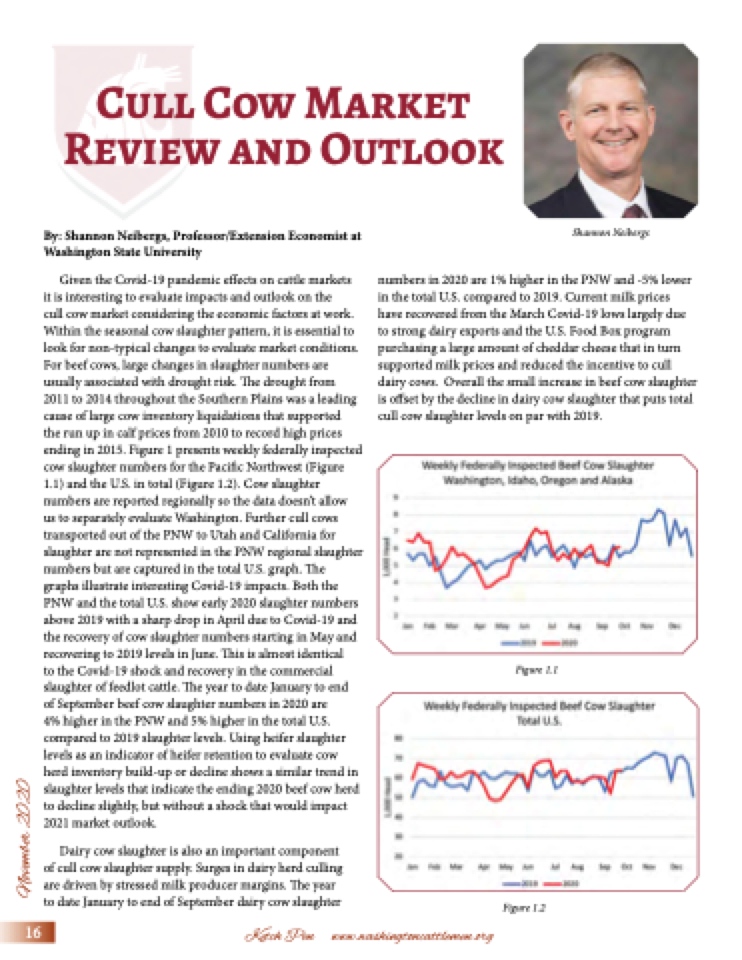

the run up in calf prices from 2010 to record high prices ending in 2015. Figure 1 presents weekly federally inspected cow slaughter numbers for the Pacific Northwest (Figure 1.1) and the U.S. in total (Figure 1.2). Cow slaughter numbers are reported regionally so the data doesn’t allow

us to separately evaluate Washington. Further cull cows transported out of the PNW to Utah and California for slaughter are not represented in the PNW regional slaughter numbers but are captured in the total U.S. graph. The graphs illustrate interesting Covid-19 impacts. Both the PNW and the total U.S. show early 2020 slaughter numbers above 2019 with a sharp drop in April due to Covid-19 and the recovery of cow slaughter numbers starting in May and recovering to 2019 levels in June. This is almost identical

to the Covid-19 shock and recovery in the commercial slaughter of feedlot cattle. The year to date January to end

of September beef cow slaughter numbers in 2020 are

4% higher in the PNW and 5% higher in the total U.S. compared to 2019 slaughter levels. Using heifer slaughter levels as an indicator of heifer retention to evaluate cow herd inventory build-up or decline shows a similar trend in slaughter levels that indicate the ending 2020 beef cow herd to decline slightly, but without a shock that would impact 2021 market outlook.

Dairy cow slaughter is also an important component of cull cow slaughter supply. Surges in dairy herd culling are driven by stressed milk producer margins. The year to date January to end of September dairy cow slaughter

Shannon Neibergs

numbers in 2020 are 1% higher in the PNW and -5% lower in the total U.S. compared to 2019. Current milk prices

have recovered from the March Covid-19 lows largely due to strong dairy exports and the U.S. Food Box program purchasing a large amount of cheddar cheese that in turn supported milk prices and reduced the incentive to cull dairy cows. Overall the small increase in beef cow slaughter is offset by the decline in dairy cow slaughter that puts total cull cow slaughter levels on par with 2019.

Figure 1.1

Figure 1.2

Ketch Pen www.washingtoncattlemen.org

November 2020