Page 10 - 06 Cotton SA September 2015

P. 10

SA Sustainable Textile and

Clothing Cluster demand study

This study, commissioned by the SA Sustainable Textile and Clothing

Cluster (now known as the Sustainable Cotton Cluster) was undertaken

by The Moss Group during 2014/15. Their final report was recently

released and some of their key findings are summarised in this article.

Background and Context aimed at turning the

he South African textile and clothing sector was South African textile

once a thriving industry capable of satisfying local and apparel industry

demand, while employing a significant number of around. Figure 2

people across the textile value chain. The situation The broader demand

Tchanged dramatically after 1994 following South study commenced with

Africa’s re-entry into the global market. During the period high-level desktop research. This was followed by a com-

1998 to 2014, local production decreased by 37% across prehensive analysis using both a bottom-up and top-down

the broader Clothing, Textile, Footwear and Leather (CTFL) research approach.

sectors, while the last six years show a substantial contraction Summary of key findings

of 28% resulting in massive job losses across the clothing

and textile sectors. The study demonstrated that the local demand for apparel

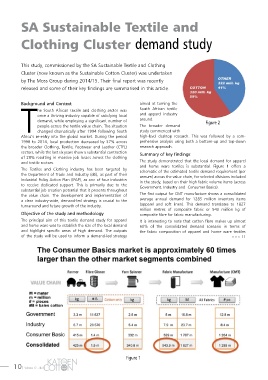

and home ware textiles is substantial. Figure 1 offers a

The Textiles and Clothing industry has been targeted by schematic of the estimated textile demand requirement (per

the Department of Trade and Industry (dti), as part of their annum) across the value chain, for selected divisions included

Industrial Policy Action Plan (IPAP), as one of four industries in the study, based on their high fabric volume items (across

to receive dedicated support. This is primarily due to the Government, Industry and Consumer Basics).

substantial job creation potential that it presents throughout

the value chain. The development and implementation of The first output for CMT manufacture shows a consolidated

a clear industry-wide, demand-led strategy is crucial to the average annual demand for 1285 million inventory items

turnaround and future growth of the industry. (apparel and soft linen). This demand translates to 1827

million metres of composite fabric or 543 million kg of

Objective of the study and methodology composite fibre for fabric manufacturing.

The principal aim of this textile demand study for apparel It is interesting to note that cotton fibre makes up almost

and home ware was to establish the size of the local demand 60% of the consolidated demand scenario in terms of

and highlight specific areas of high demand. The outputs the fabric composition of apparel and home ware textiles

of the study will be used to inform a demand-led strategy >>> 11

Figure 1

10 | Volume 17 – No 2