Page 9 - FSUOGM Week 46

P. 9

FSUOGM COMMENTARY FSUOGM

shortly after that.

Another 10 bcm per year project in Nord Stream 2 will indeed diversify Ger-

Brunsbuettel, led by Germany’s Uniper, showed many’s gas supply, at least in terms of import

initial promise when ExxonMobil reached a pro- routes, while also lowering costs due to the

visional deal to book a large portion of its capac- lack of transit countries. Russia has three main

ity in 2019. But its fate is now up in the air. options for ramping up supplies to Europe – in

Uniper said on November 6 it was reviewing the form of LNG, via Ukraine and via the Turk-

the plan and might decide to convert the pro- Stream to Turkey. But Moscow is eager to stop

posed facility to import hydrogen. The move using the Ukrainian route once its five-year con-

comes after Uniper’s call for binding bids for tract expires in 2025. Meanwhile, the smaller

the project’s capacity ended in disappointing Yamal-Europe pipeline through Poland and

interest. Belarus will require upgrades, further strength-

Australian investment bank Macquarie and ening the case for Nord Stream 2.

ChinaHarbour Engineering, want to build a 5-8 The best scenario for Germany may be to

bcm per year plant in Stade, but this project is at pursue both Nord Stream 2 and its own regas-

an even less advanced stage. ification capacity.

“We see Gazprom benefiting from the Nord

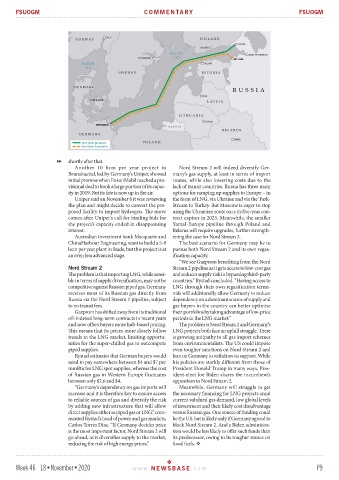

Nord Stream 2 Stream 2 pipeline as it gets access to low-cost gas

The problem is that importing LNG, while sensi- and reduces supply risk in bypassing third-party

ble in terms of supply diversification, may not be countries,” Rystad concluded. “Having access to

competitive against Russian piped gas. Germany LNG through their own regasification termi-

receives most of its Russian gas directly from nals will additionally allow Germany to reduce

Russia via the Nord Stream 1 pipeline, subject dependency on a dominant source of supply and

to no transit fees. gas buyers in the country can better optimise

Gazprom has shifted away from its traditional their portfolios by taking advantage of low-price

oil-indexed long-term contracts in recent years periods in the LNG market.”

and now offers buyers more hub-based pricing. The problem is Nord Stream 2 and Germany’s

This means that its prices more closely follow LNG projects both face an uphill struggle. There

trends in the LNG market, limiting opportu- is growing antipathy to all gas import schemes

nities for the super-chilled gas to outcompete from environmentalists. The US could impose

piped supplies. even tougher sanctions on Nord Stream 2 and

Rystad estimates that German buyers would lean on Germany to withdraw its support. While

need to pay somewhere between $4 and $7 per his policies are starkly different from those of

mmBtu for LNG spot supplies, whereas the cost President Donald Trump in many ways, Pres-

of Russian gas in Western Europe fluctuates ident-elect Joe Biden shares the incumbent’s

between only $2.6 and $4. opposition to Nord Stream 2.

“Germany’s dependency on gas imports will Meanwhile, Germany will struggle to get

increase and it is therefore key to ensure access the necessary financing for LNG projects amid

to reliable sources of gas and diversify the risk current subdued gas demand, low global levels

by adding new infrastructure that will allow of investment and their likely cost disadvantage

direct supplies either as piped gas or LNG,” com- versus Russian gas. One source of funding could

mented Rystad’s head of power and gas markets, be the US, but is likely only if Germany agreed to

Carlos Torres Diaz. “If Germany decides price block Nord Stream 2. And a Biden administra-

is the most important factor, Nord Stream 2 will tion would be less likely to offer such funds than

go ahead, as it diversifies supply to the market, its predecessor, owing to its tougher stance on

reducing the risk of high energy prices.” fossil fuels.

Week 46 18•November•2020 www. NEWSBASE .com P9