Page 106 - ITGC_Audit Guides

P. 106

Objectives

This guide is intended to help the reader:

• Define business applications and obtain a working knowledge of relevant processes,

including related administrative and operational controls.

• Understand risks and opportunities associated with business applications.

• Understand components of the system development life cycle, including:

o Coding to meet operational and security requirements.

o Testing for security and functionality.

o Controlling the release and storage of source code.

o Installing security patches and other updates.

• Understand components of production support, including:

o Configuring the application and connections to external systems.

o Administering system roles and accounts.

o Responding to user and operational feedback, including errors and outages.

• Understand some related controls for documentation, vendor management, asset

management, and reporting from application databases.

• Understand approaches to auditing business applications, including specific controls that

should be present and evaluated.

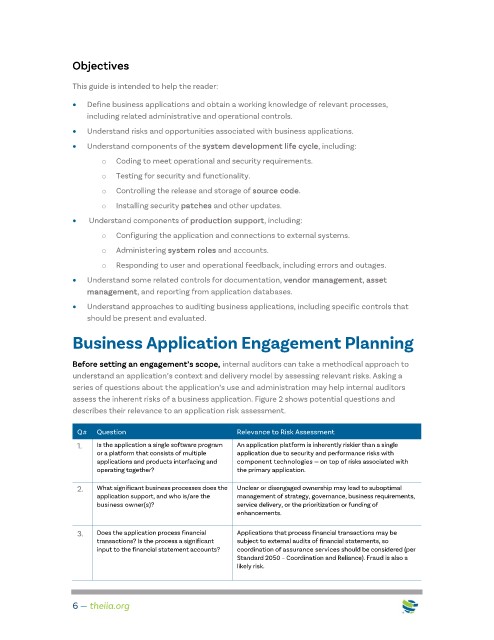

Business Application Engagement Planning

Before setting an engagement’s scope, internal auditors can take a methodical approach to

understand an application’s context and delivery model by assessing relevant risks. Asking a

series of questions about the application’s use and administration may help internal auditors

assess the inherent risks of a business application. Figure 2 shows potential questions and

describes their relevance to an application risk assessment.

Q# Question Relevance to Risk Assessment

1. Is the application a single software program An application platform is inherently riskier than a single

or a platform that consists of multiple application due to security and performance risks with

applications and products interfacing and component technologies — on top of risks associated with

operating together? the primary application.

2. What significant business processes does the Unclear or disengaged ownership may lead to suboptimal

application support, and who is/are the management of strategy, governance, business requirements,

business owner(s)? service delivery, or the prioritization or funding of

enhancements.

3. Does the application process financial Applications that process financial transactions may be

transactions? Is the process a significant subject to external audits of financial statements, so

input to the financial statement accounts? coordination of assurance services should be considered (per

Standard 2050 – Coordination and Reliance). Fraud is also a

likely risk.

6 — theiia.org