Page 508 - Auditing Standards

P. 508

As of December 15, 2017

statements presented, an auditor may express a qualified or adverse opinion, disclaim an opinion, or include

an explanatory paragraph with respect to one or more financial statements for one or more periods, while

issuing a different report on the other financial statements presented. Following are examples of reports on

comparative financial statements with different reports on one or more financial statements presented.

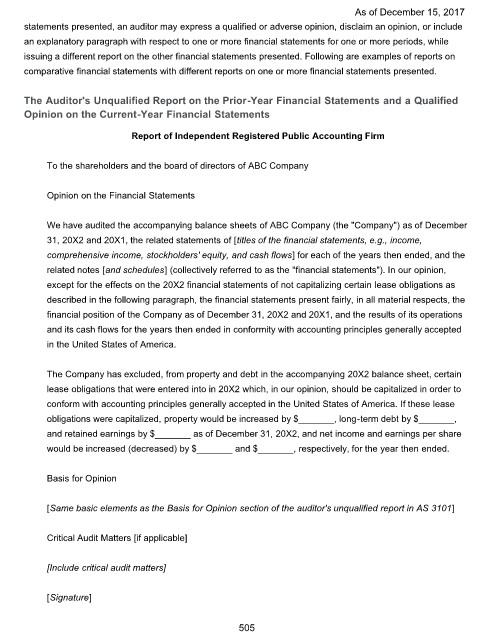

The Auditor's Unqualified Report on the Prior-Year Financial Statements and a Qualified

Opinion on the Current-Year Financial Statements

Report of Independent Registered Public Accounting Firm

To the shareholders and the board of directors of ABC Company

Opinion on the Financial Statements

We have audited the accompanying balance sheets of ABC Company (the "Company") as of December

31, 20X2 and 20X1, the related statements of [titles of the financial statements, e.g., income,

comprehensive income, stockholders' equity, and cash flows] for each of the years then ended, and the

related notes [and schedules] (collectively referred to as the "financial statements"). In our opinion,

except for the effects on the 20X2 financial statements of not capitalizing certain lease obligations as

described in the following paragraph, the financial statements present fairly, in all material respects, the

financial position of the Company as of December 31, 20X2 and 20X1, and the results of its operations

and its cash flows for the years then ended in conformity with accounting principles generally accepted

in the United States of America.

The Company has excluded, from property and debt in the accompanying 20X2 balance sheet, certain

lease obligations that were entered into in 20X2 which, in our opinion, should be capitalized in order to

conform with accounting principles generally accepted in the United States of America. If these lease

obligations were capitalized, property would be increased by $_______, long-term debt by $_______,

and retained earnings by $_______ as of December 31, 20X2, and net income and earnings per share

would be increased (decreased) by $_______ and $_______, respectively, for the year then ended.

Basis for Opinion

[Same basic elements as the Basis for Opinion section of the auditor's unqualified report in AS 3101]

Critical Audit Matters [if applicable]

[Include critical audit matters]

[Signature]

505