Page 622 - Large Business IRS Training Guides

P. 622

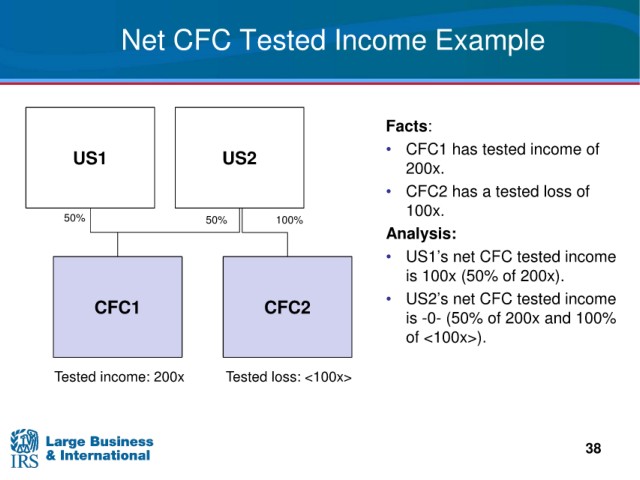

Net

CFC Tested Income Example

Facts:

• CFC1 has

tested income of

US1

US2

200x.

• CFC2 has

a tested loss of

100x.

50% 50% 100%

Analysis:

net CFC tested income

• US1’s

(50% of 200x).

is 100x

net CFC tested income

• US2’s

CFC1 CFC2

is -0- (50% of 200x and 100%

of <100x>).

Tested income: 200x Tested loss: <100x>

38