Page 164 - International Taxation IRS Training Guides

P. 164

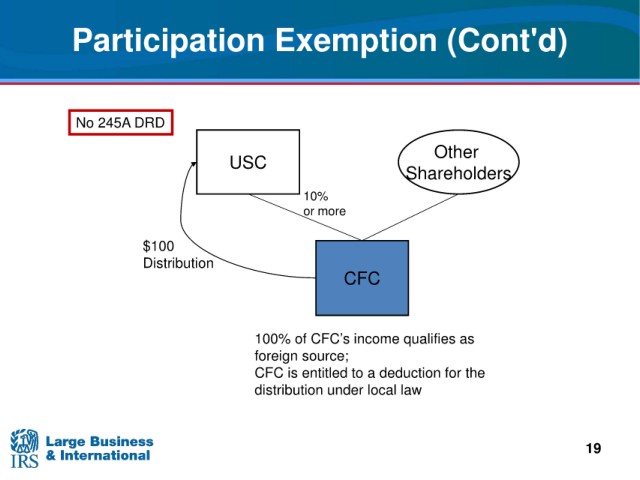

Participation Exemption (Cont'd)

No 245A DRD

Other

USC

Shareholders

10%

or more

$100

Distribution

CFC

100% of CFC’s income qualifies as

foreign source;

CFC is

entitled to a deduction for the

distribution under local law

19