Page 73 - Intellectual Property Disputes

P. 73

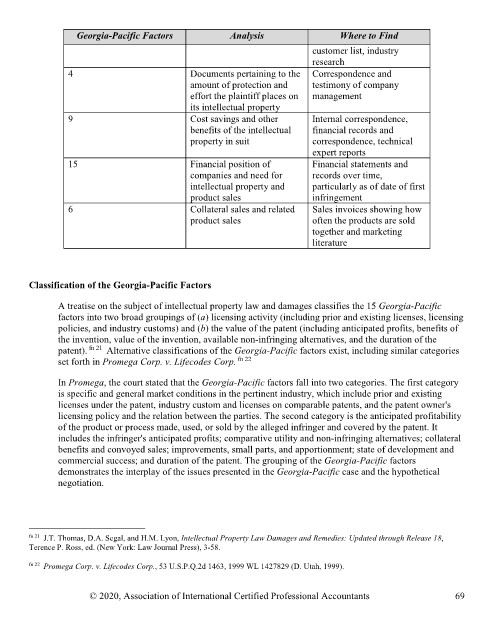

Georgia-Pacific Factors Analysis Where to Find

customer list, industry

research

4 Documents pertaining to the Correspondence and

amount of protection and testimony of company

effort the plaintiff places on management

its intellectual property

9 Cost savings and other Internal correspondence,

benefits of the intellectual financial records and

property in suit correspondence, technical

expert reports

15 Financial position of Financial statements and

companies and need for records over time,

intellectual property and particularly as of date of first

product sales infringement

6 Collateral sales and related Sales invoices showing how

product sales often the products are sold

together and marketing

literature

Classification of the Georgia-Pacific Factors

A treatise on the subject of intellectual property law and damages classifies the 15 Georgia-Pacific

factors into two broad groupings of (a) licensing activity (including prior and existing licenses, licensing

policies, and industry customs) and (b) the value of the patent (including anticipated profits, benefits of

the invention, value of the invention, available non-infringing alternatives, and the duration of the

patent). fn 21 Alternative classifications of the Georgia-Pacific factors exist, including similar categories

set forth in Promega Corp. v. Lifecodes Corp. fn 22

In Promega, the court stated that the Georgia-Pacific factors fall into two categories. The first category

is specific and general market conditions in the pertinent industry, which include prior and existing

licenses under the patent, industry custom and licenses on comparable patents, and the patent owner's

licensing policy and the relation between the parties. The second category is the anticipated profitability

of the product or process made, used, or sold by the alleged infringer and covered by the patent. It

includes the infringer's anticipated profits; comparative utility and non-infringing alternatives; collateral

benefits and convoyed sales; improvements, small parts, and apportionment; state of development and

commercial success; and duration of the patent. The grouping of the Georgia-Pacific factors

demonstrates the interplay of the issues presented in the Georgia-Pacific case and the hypothetical

negotiation.

fn 21 J.T. Thomas, D.A. Segal, and H.M. Lyon, Intellectual Property Law Damages and Remedies: Updated through Release 18,

Terence P. Ross, ed. (New York: Law Journal Press), 3-58.

fn 22 Promega Corp. v. Lifecodes Corp., 53 U.S.P.Q.2d 1463, 1999 WL 1427829 (D. Utah, 1999).

© 2020, Association of International Certified Professional Accountants 69