Page 292 - IC38 GENERAL INSURANCE

P. 292

Mr. Shyam‘s position

The probability of loss (0.007) is of little use to Mr. Shyam since it only suggests

that on average about 7 out of 1000 factories like his, would be impacted by the

loss. He does not know whether his factory would be one among the unfortunate

seven? In fact nobody can predict if the particular factory would suffer a loss.

Shyam may be said to be in a state of uncertainty. Not only does he not know

the future, he cannot even predict what it will be. It is obviously a cause for

anxiety.

Insurer‘s position

Let us now look at the insurer‟s position. When Shyam‟s risk of loss is combined

and pooled with that of thousands of others, who are exposed to similar

situation, it now becomes finite and predictable.

The insurer need not worry about Shyam‟s factory as much as the latter does. It

is enough that only seven out of thousand factories be subjected to the loss.

So long as the actual losses are same or nearly same as the expected, the

insurer can meet them by drawing money from the pool of funds.

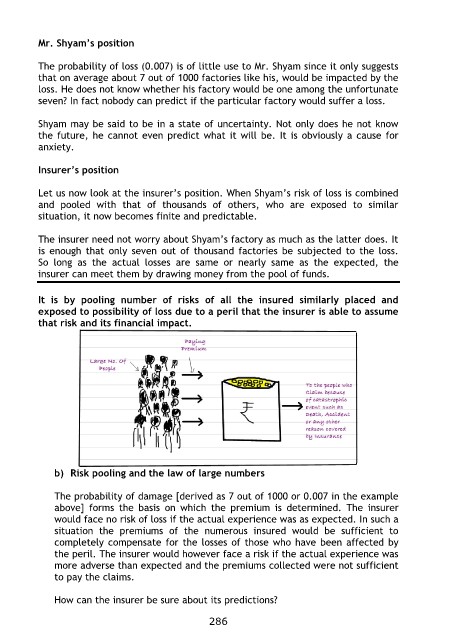

It is by pooling number of risks of all the insured similarly placed and

exposed to possibility of loss due to a peril that the insurer is able to assume

that risk and its financial impact.

b) Risk pooling and the law of large numbers

The probability of damage [derived as 7 out of 1000 or 0.007 in the example

above] forms the basis on which the premium is determined. The insurer

would face no risk of loss if the actual experience was as expected. In such a

situation the premiums of the numerous insured would be sufficient to

completely compensate for the losses of those who have been affected by

the peril. The insurer would however face a risk if the actual experience was

more adverse than expected and the premiums collected were not sufficient

to pay the claims.

How can the insurer be sure about its predictions?

286