Page 28 - Insurance Times April 2022

P. 28

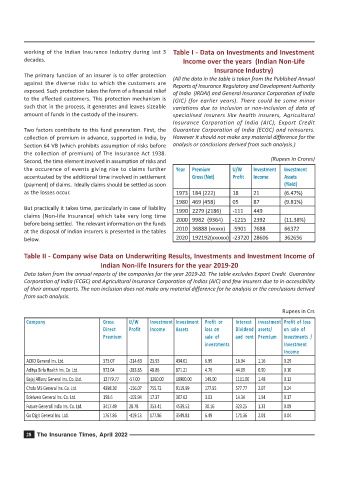

working of the Indian Insurance Industry during last 3 Table I - Data on Investments and Investment

decades. Income over the years (Indian Non-Life

Insurance Industry)

The primary function of an insurer is to offer protection

(All the data in the table is taken from the Published Annual

against the diverse risks to which the customers are

Reports of Insurance Regulatory and Development Authority

exposed. Such protection takes the form of a financial relief of India (IRDAI) and General Insurance Corporation of India

to the affected customers. This protection mechanism is (GIC) (for earlier years). There could be some minor

such that in the process, it generates and leaves sizeable variations due to inclusion or non-inclusion of data of

amount of funds in the custody of the insurers. specialised insurers like health insurers, Agricultural

Insurance Corporation of India (AIC), Export Credit

Two factors contribute to this fund generation. First, the Guarantee Corporation of India (ECGC) and reinsurers.

collection of premium in advance, supported in India, by However it should not make any material difference for the

Section 64 VB (which prohibits assumption of risks before analysis or conclusions derived from such analysis.)

the collection of premium) of The Insurance Act 1938.

Second, the time element involved in assumption of risks and (Rupees in Crores)

the occurence of events giving rise to claims further Year Premium U/W Investment Investment

accentuated by the additional time involved in settlement Gross (Net) Profit Income Assets

(payment) of claims. Ideally claims should be settled as soon (Yield)

as the losses occur. 1973 184 (222) 18 21 (6.47%)

1980 469 (458) 05 87 (9.81%)

But practically it takes time, particularly in case of liability

1990 2279 (2186) -111 449

claims (Non-life Insurance) which take very long time

2000 9982 (9364) -1215 2392 (11.38%)

before being settled. The relevant information on the funds

2010 36888 (xxxxx) -5901 7688 66372

at the disposal of Indian insurers is presented in the tables

below. 2020 192192(xxxxxx) -23720 28606 362656

Table II - Company wise Data on Underwriting Results, Investments and Investment Income of

Indian Non-life Insurers for the year 2019-20

Data taken from the annual reports of the companies for the year 2019-20. The table excludes Export Credit Guarantee

Corporation of India (ECGC) and Agricultural Insurance Corporation of Indias (AIC) and few insurers due to in-accessibility

of their annual reports. The non inclusion does not make any material difference for he analysis or the conclusions derived

from such analysis.

Rupees in Crs

Company Gross U/W Investment Investment Profit or Interest investment Profit of loss

Direct Profit Income Assets loss on Dividend assets/ on sale of

Premium sale of and rent Premium Investments /

investments Investment

Income

ACKO General Ins. Ltd. 373.07 -214.63 23.93 434.01 6.99 16.94 1.16 0.29

Aditya Birla Health Ins. Co. Ltd. 972.04 -283.85 48.86 871.21 4.76 44.09 0.90 0.10

Bajaj Allianz General Ins. Co. Ltd. 12779.77 -57.00 1260.00 18900.00 149.00 1111.00 1.48 0.12

Chola MS General Ins. Co. Ltd. 4398.30 -156.07 755.72 9119.99 177.95 577.77 2.07 0.24

Edelweis General Ins. Co. Ltd. 158.6 -102.94 17.37 307.62 3.03 14.34 1.94 0.17

Future Generali India Ins. Co. Ltd. 3417.49 28.78 353.41 4539.52 30.16 323.25 1.33 0.09

Go Digit General Ins. Ltd. 1767.86 -419.13 177.86 3549.81 6.49 171.36 2.01 0.04

28 The Insurance Times, April 2022