Page 42 - MAZOO EBOOK 1_Neat

P. 42

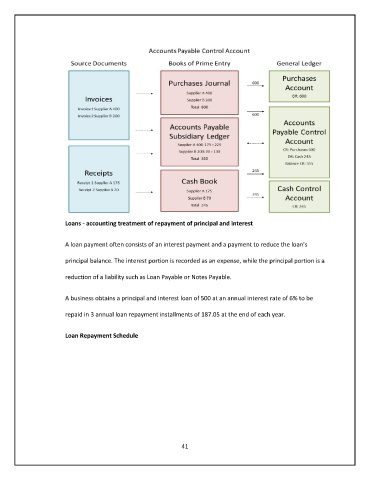

Loans - accounting treatment of repayment of principal and interest

A loan payment often consists of an interest payment and a payment to reduce the loan’s

principal balance. The interest portion is recorded as an expense, while the principal portion is a

reduction of a liability such as Loan Payable or Notes Payable.

A business obtains a principal and interest loan of 500 at an annual interest rate of 6% to be

repaid in 3 annual loan repayment installments of 187.05 at the end of each year.

Loan Repayment Schedule

41