Page 2 - BI 2018 Benefits Related to Uniform definition of a child

P. 2

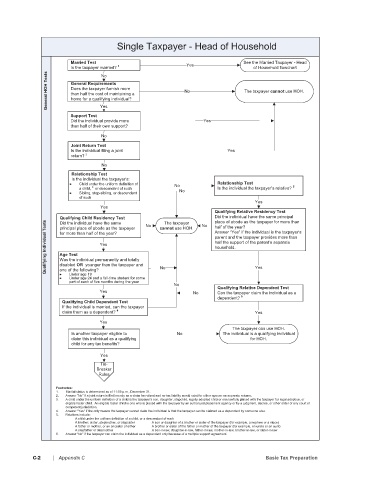

Married Test See the Married Taxpayer - Head

Is the taxpayer married? 1 Yes of Household flowchart

General HOH Tests General Requirements No The taxpayer cannot use HOH.

No

Does the taxpayer furnish more

than half the cost of maintaining a

home for a qualifying individual?

Support Test Yes

Did the individual provide more Yes

than half of their own support?

No

Joint Return Test

Is the individual filing a joint Yes

return? 2

No

Relationship Test

Is the individual the taxpayer’s:

Child under the uniform definition of No Relationship Test

3

a child, or descendant of such No Is the individual the taxpayer’s relative? 5

Sibling, step-sibling, or descendant

of such

Yes

Yes

Qualifying Relative Residency Test

Qualifying Child Residency Test No cannot use HOH. No Did the individual have the same principal

place of abode as the taxpayer for more than

Qualifying Individual Tests for more than half of the year? parent and the taxpayer provides more than

Did the individual have the same

The taxpayer

half of the year?

principal place of abode as the taxpayer

Answer “Yes” if the individual is the taxpayer’s

half the support of the parent’s separate

Yes

household.

Age Test

Was the individual permanently and totally

disabled OR younger than the taxpayer and

one of the following?

Under age 19

Under age 24 and a full-time student for some No Yes

part of each of five months during the year

No

Qualifying Relative Dependent Test

Yes No Can the taxpayer claim the individual as a

dependent? 6

Qualifying Child Dependent Test

If the individual is married, can the taxpayer

claim them as a dependent? 4 Yes

Yes

The taxpayer can use HOH.

Is another taxpayer eligible to No The individual is a qualifying individual

claim this individual as a qualifying for HOH.

child for any tax benefits?

Yes

Tie-

Breaker

Rules

Footnotes:

1. Marital status is determined as of 11:59 p.m., December 31.

2. Answer “No” if a joint return is filed merely as a claim for refund and no tax liability would exist for either spouse on separate returns.

3. A child under the uniform definition of a child is the taxpayer's son, daughter, stepchild, legally adopted child or one lawfully placed with the taxpayer for legal adoption, or

eligible foster child. An eligible foster child is one who is placed with the taxpayer by an authorized placement agency or by a judgment, decree, or other order of any court of

competent jurisdiction.

4. Answer "Yes" if the only reason the taxpayer cannot claim the individual is that the taxpayer can be claimed as a dependent by someone else.

5. Relatives include:

A child under the uniform definition of a child, or a descendant of such

A brother, sister, stepbrother, or stepsister A son or daughter of a brother or sister of the taxpayer (for example, a nephew or a niece)

A father or mother, or an ancestor of either A brother or sister of the father or mother of the taxpayer (for example, an uncle or an aunt)

A stepfather or stepmother A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

6. Answer “No” if the taxpayer can claim the individual as a dependent only because of a multiple support agreement.

C-2 | Appendix C Basic Tax Preparation