Page 7 - P6 Slide Taxation - Lecture Day 5 - Groups

P. 7

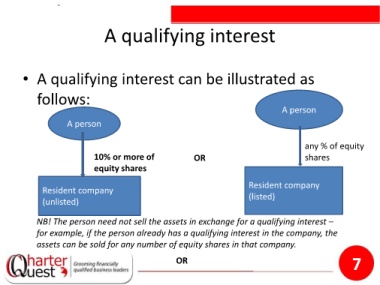

A qualifying interest

• A qualifying interest can be illustrated as

follows:

A person

A person

any % of equity

10% or more of OR shares

equity shares

Resident company

Resident company

(unlisted) (listed)

NB! The person need not sell the assets in exchange for a qualifying interest –

for example, if the person already has a qualifying interest in the company, the

assets can be sold for any number of equity shares in that company.

OR 7