Page 158 - AAA Integrated Workbook STUDENT S18-J19

P. 158

Chapter 103 4

Subsequent events

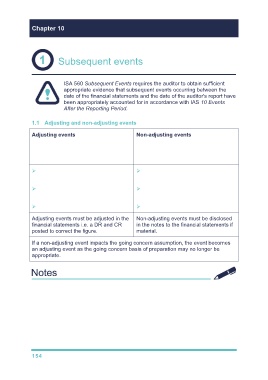

ISA 560 Subsequent Events requires the auditor to obtain sufficient

appropriate evidence that subsequent events occurring between the

date of the financial statements and the date of the auditor's report have

been appropriately accounted for in accordance with IAS 10 Events

After the Reporting Period.

1.1 Adjusting and non-adjusting events

Adjusting events Non-adjusting events

Provide additional evidence about Provide evidence about conditions

conditions existing at the statement of arising after the statement of financial

financial position date. position date.

Trade receivables become Fire destroys inventory after the

irrecoverable debts year-end

Inventory held at year-end is sold Injury resulting in legal action

for less than cost after year-end occurs after year-end

Estimate for a provision is revised Takeover

Adjusting events must be adjusted in the Non-adjusting events must be disclosed

financial statements i.e. a DR and CR in the notes to the financial statements if

posted to correct the figure. material.

If a non-adjusting event impacts the going concern assumption, the event becomes

an adjusting event as the going concern basis of preparation may no longer be

appropriate.

154