Page 243 - AAA Integrated Workbook STUDENT S18-J19

P. 243

Forensic audits

Definitions

Forensic audit refers to the specific procedures used to obtain

evidence, usually to quantify a financial loss.

This could include the use of traditional financial auditing techniques

such as analytical procedures and substantive procedures for example

to quantify the extent of a fraud or to determine the amount of an

insurance claim.

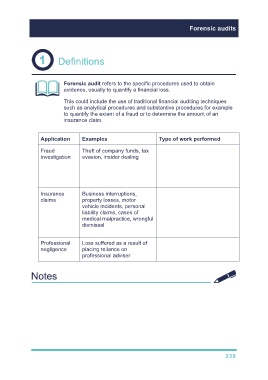

Application Examples Type of work performed

Fraud Theft of company funds, tax Funds tracing, asset

investigation evasion, insider dealing identification and recovery,

forensic intelligence gathering,

due diligence reviews,

interviews, detailed review of

documentary evidence

Insurance Business interruptions, Detailed review of the policy

claims property losses, motor from either an insured or

vehicle incidents, personal insurer’s perspective to

liability claims, cases of investigate coverage issues,

medical malpractice, wrongful identification of appropriate

dismissal method of calculating the loss,

quantification of losses

Professional Loss suffered as a result of Advising on merits of a case in

negligence placing reliance on regards to liability, quantifying

professional adviser losses

239