Page 36 - AAA Integrated Workbook STUDENT S18-J19

P. 36

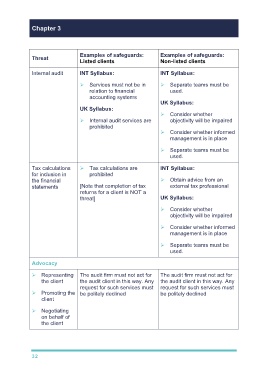

Chapter 3

Examples of safeguards: Examples of safeguards:

Threat

Listed clients Non-listed clients

Internal audit INT Syllabus: INT Syllabus:

Services must not be in Separate teams must be

relation to financial used.

accounting systems

UK Syllabus:

UK Syllabus:

Consider whether

Internal audit services are objectivity will be impaired

prohibited

Consider whether informed

management is in place

Separate teams must be

used.

Tax calculations Tax calculations are INT Syllabus:

for inclusion in prohibited

the financial Obtain advice from an

statements [Note that completion of tax external tax professional

returns for a client is NOT a

threat] UK Syllabus:

Consider whether

objectivity will be impaired

Consider whether informed

management is in place

Separate teams must be

used.

Advocacy

Representing The audit firm must not act for The audit firm must not act for

the client the audit client in this way. Any the audit client in this way. Any

request for such services must request for such services must

Promoting the be politely declined be politely declined

client

Negotiating

on behalf of

the client

32