Page 67 - BA2 Integrated Workbook - Student 2017

P. 67

Overhead analysis

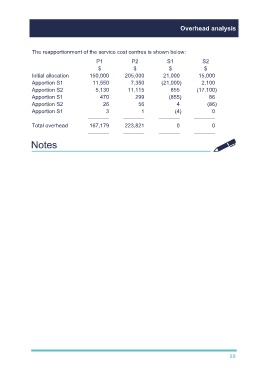

The reapportionment of the service cost centres is shown below:

P1 P2 S1 S2

$ $ $ $

Initial allocation 150,000 205,000 21,000 15,000

Apportion S1 11,550 7,350 (21,000) 2,100

Apportion S2 5,130 11,115 855 (17,100)

Apportion S1 470 299 (855) 86

Apportion S2 26 56 4 (86)

Apportion S1 3 1 (4) 0

––––––– ––––––– ––––––– –––––––

Total overhead 167,179 223,821 0 0

––––––– ––––––– ––––––– –––––––

59