Page 101 - SBR Integrated Workbook STUDENT S18-J19

P. 101

Leases

Lessee accounting

2.1 Measurement

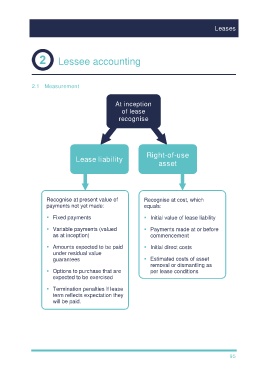

At inception

of lease

recognise

Right-of-use

Lease liability

asset

Recognise at present value of Recognise at cost, which

payments not yet made: equals:

Fixed payments Initial value of lease liability

Variable payments (valued Payments made at or before

as at inception) commencement

Amounts expected to be paid Initial direct costs

under residual value

guarantees Estimated costs of asset

removal or dismantling as

Options to purchase that are per lease conditions

expected to be exercised

Termination penalties if lease

term reflects expectation they

will be paid.

95