Page 278 - SBR Integrated Workbook STUDENT S18-J19

P. 278

Chapter 18

Joint arrangements

7.1 Definitions

Joint arrangements are defined as ‘arrangements where two or

more parties have joint control’ (IFRS 11, Appendix A). This will only

apply if the relevant activities require unanimous consent of those who

collectively control the arrangement.

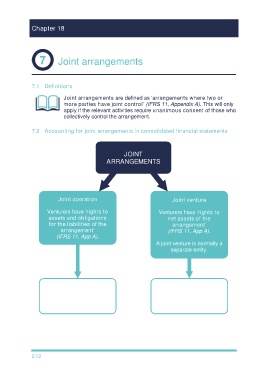

7.2 Accounting for joint arrangements in consolidated financial statements

JOINT

ARRANGEMENTS

Joint operation Joint venture

Venturers have ‘rights to Venturers have ‘rights to

assets and obligations net assets of the

for the liabilities of the arrangement’

arrangement’ (IFRS 11, App A).

(IFRS 11, App A).

A joint venture is normally a

separate entity.

Account for share of Equity account

assets, liabilities, incomes

and expenses. (same as associates)

272