Page 310 - SBR Integrated Workbook STUDENT S18-J19

P. 310

Chapter 20

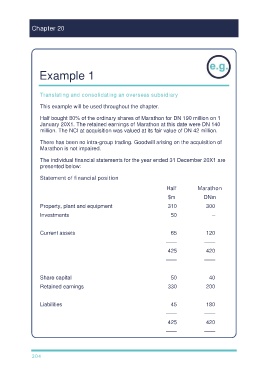

Example 1

Translating and consolidating an overseas subsidiary

This example will be used throughout the chapter.

Half bought 80% of the ordinary shares of Marathon for DN 190 million on 1

January 20X1. The retained earnings of Marathon at this date were DN 140

million. The NCI at acquisition was valued at its fair value of DN 42 million.

There has been no intra-group trading. Goodwill arising on the acquisition of

Marathon is not impaired.

The individual financial statements for the year ended 31 December 20X1 are

presented below:

Statement of financial position

Half Marathon

$m DNm

Property, plant and equipment 310 300

Investments 50 –

Current assets 65 120

—— ——

425 420

—— ——

Share capital 50 40

Retained earnings 330 200

Liabilities 45 180

—— ——

425 420

—— ——

304