Page 182 - Microsoft Word - 00 P1 IW Prelims.docx

P. 182

Chapter 11

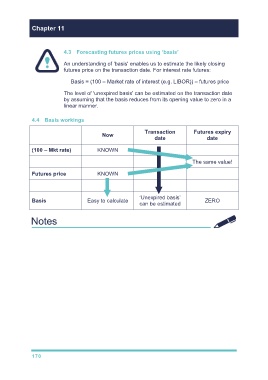

4.3 Forecasting futures prices using ‘basis’

An understanding of 'basis' enables us to estimate the likely closing

futures price on the transaction date. For interest rate futures:

Basis = (100 – Market rate of interest (e.g. LIBOR)) – futures price

The level of 'unexpired basis' can be estimated on the transaction date

by assuming that the basis reduces from its opening value to zero in a

linear manner.

4.4 Basis workings

Transaction Futures expiry

Now

date date

(100 – Mkt rate) KNOWN

The same value!

Futures price KNOWN

‘Unexpired basis’

Basis Easy to calculate ZERO

can be estimated

170