Page 21 - APM Integrated Workbook STUDENT S18-J19

P. 21

Introduction to strategic management accounting

The changing role of the management

accountant

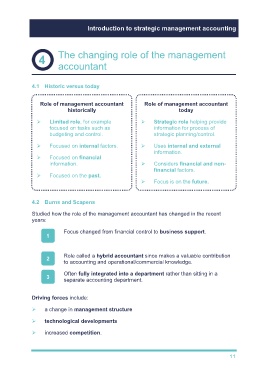

4.1 Historic versus today

Role of management accountant Role of management accountant

historically today

Limited role, for example Strategic role helping provide

focused on tasks such as information for process of

budgeting and control. strategic planning/control.

Focused on internal factors. Uses internal and external

information.

Focused on financial

information. Considers financial and non-

financial factors.

Focused on the past.

Focus is on the future.

4.2 Burns and Scapens

Studied how the role of the management accountant has changed in the recent

years:

Focus changed from financial control to business support. For

1 example, how to get the most out of the MIS or developing a range of

KPIs.

Role called a hybrid accountant since makes a valuable contribution

2

to accounting and operational/commercial knowledge.

Often fully integrated into a department rather than sitting in a

3

separate accounting department.

Driving forces include:

a change in management structure

technological developments

increased competition.

11