Page 102 - Microsoft Word - 00 IWB ACCA F7.docx

P. 102

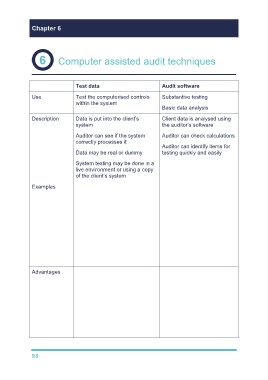

Chapter 6 3 4

Computer assisted audit techniques

Test data Audit software

Use Test the computerised controls Substantive testing

within the system

Basic data analysis

Description Data is put into the client’s Client data is analysed using

system the auditor’s software

Auditor can see if the system Auditor can check calculations

correctly processes it

Auditor can identify items for

Data may be real or dummy testing quickly and easily

System testing may be done in a

live environment or using a copy

of the client’s system

Examples The auditor enters data e.g. Re-performance of

addition or ageing of

A timesheet with hours invoices

outside the normal range to

check that the system Identifying items for

rejects it. testing e.g. identify credit

balances on the

A customer order that will receivables ledger

exceed the credit limit to

ensure the system rejects it. Preparation of reports

Calculations of ratios

Sample selection

Advantages Enables the auditor to test Calculations and casting

programmed controls which of reports will be quicker.

wouldn't otherwise be able

to be tested. More transactions can be

tested

Once designed, costs

incurred will be minimal Computer files rather

unless the programmed than printouts are tested

controls are changed Cost effective once set

requiring the test data to be up

redesigned.

98