Page 30 - Microsoft Word - 00 IWB ACCA F7.docx

P. 30

Chapter 3

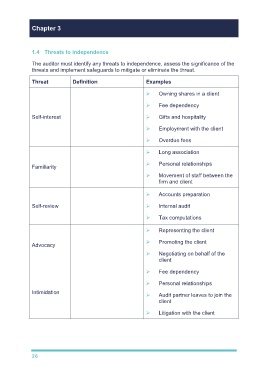

1.4 Threats to independence

The auditor must identify any threats to independence, assess the significance of the

threats and implement safeguards to mitigate or eliminate the threat.

Threat Definition Examples

Owning shares in a client

Where the auditor has a Fee dependency

financial or other interest

Self-interest that will inappropriately Gifts and hospitality

influence their judgment or

behaviour Employment with the client

Overdue fees

Long association

The auditor becomes too

sympathetic to or trusting of Personal relationships

Familiarity

a client and loses

professional scepticism Movement of staff between the

firm and client

The auditor will be unlikely Accounts preparation

to admit to errors in their

Self-review own work, or may not Internal audit

identify the errors in their

own work Tax computations

Representing the client

Promoting the position of

Advocacy the client or representing Promoting the client

them in some way Negotiating on behalf of the

client

Fee dependency

Actual or perceived

pressures from the client, or Personal relationships

Intimidation attempts to exercise undue Audit partner leaves to join the

influence over the client

assurance provider

Litigation with the client

26