Page 36 - Microsoft Word - 00 IWB ACCA F7.docx

P. 36

Chapter 3

Acceptance

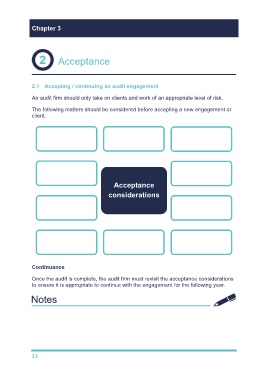

2.1 Accepting / continuing an audit engagement

An audit firm should only take on clients and work of an appropriate level of risk.

The following matters should be considered before accepting a new engagement or

client.

Professional Independence Management

clearance & objectivity integrity

Preconditions Money

for an audit laundering

Acceptance

considerations

Reputation of

Resources

the client

Professional

Fees Risks

competence

Continuance

Once the audit is complete, the audit firm must revisit the acceptance considerations

to ensure it is appropriate to continue with the engagement for the following year.

32