Page 53 - Microsoft Word - 00 IWB ACCA F7.docx

P. 53

Risk

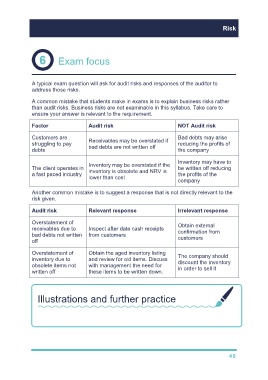

Exam focus

A typical exam question will ask for audit risks and responses of the auditor to

address those risks.

A common mistake that students make in exams is to explain business risks rather

than audit risks. Business risks are not examinable in this syllabus. Take care to

ensure your answer is relevant to the requirement.

Factor Audit risk NOT Audit risk

Customers are Receivables may be overstated if Bad debts may arise

struggling to pay reducing the profits of

debts bad debts are not written off the company

Inventory may have to

Inventory may be overstated if the

The client operates in inventory is obsolete and NRV is be written off reducing

a fast paced industry the profits of the

lower than cost

company

Another common mistake is to suggest a response that is not directly relevant to the

risk given.

Audit risk Relevant response Irrelevant response

Overstatement of Obtain external

receivables due to Inspect after date cash receipts confirmation from

bad debts not written from customers customers

off

Overstatement of Obtain the aged inventory listing The company should

inventory due to and review for old items. Discuss discount the inventory

obsolete items not with management the need for in order to sell it

written off these items to be written down.

Illustrations and further practice

Now try TYU question 1 from Chapter 4

49