Page 61 - Microsoft Word - 00 IWB ACCA F7.docx

P. 61

Planning

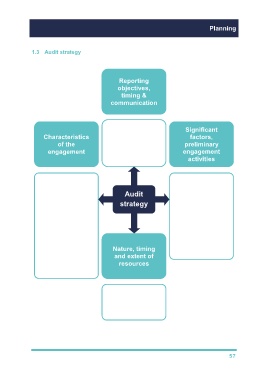

1.3 Audit strategy

Reporting

objectives,

timing &

communication

Timetable for Significant

reporting

Characteristics factors,

of the Communication preliminary

engagement with client, team & engagement

3 parties activities

rd

FR framework Materiality

Industry reporting Audit Risk assessment

Knowledge of strategy Internal controls

business Need for

scepticism

Internal audit

Changes in laws &

Service regulations

organisation Significant

Nature, timing

Use of CAATs developments

and extent of

resources

Availability of client

staff

Selection of audit

team

Budget

57