Page 7 - Microsoft Word - 00 IWB ACCA F7.docx

P. 7

Introduction to assurance

Elements of assurance

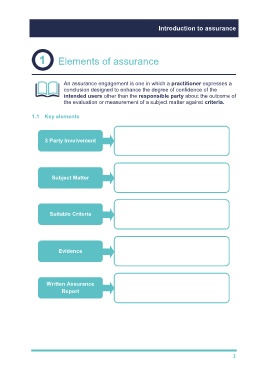

An assurance engagement is one in which a practitioner expresses a

conclusion designed to enhance the degree of confidence of the

intended users other than the responsible party about the outcome of

the evaluation or measurement of a subject matter against criteria.

1.1 Key elements

Practitioner

3 Party Involvement Intended user

Responsible party

E.g. financial statements, other

Subject Matter

financial data, systems

E.g. accounting standards,

Suitable Criteria

UK Corporate Governance Code

Evidence Sufficient and appropriate

Written Assurance Expressing a conclusion or opinion

Report

3