Page 37 - FINAL CFA I SLIDES JUNE 2019 DAY 6

P. 37

Session Unit 5:

20. Currency Exchange Rates

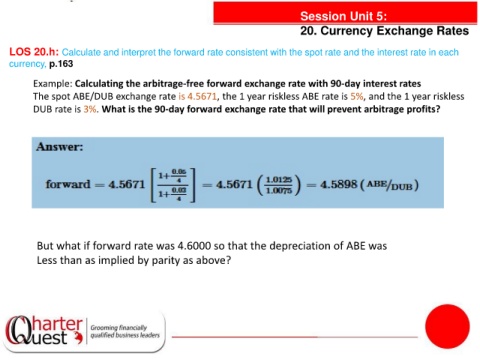

LOS 20.h: Calculate and interpret the forward rate consistent with the spot rate and the interest rate in each

currency, p.163

Example: Calculating the arbitrage-free forward exchange rate with 90-day interest rates

The spot ABE/DUB exchange rate is 4.5671, the 1 year riskless ABE rate is 5%, and the 1 year riskless

DUB rate is 3%. What is the 90-day forward exchange rate that will prevent arbitrage profits?

But what if forward rate was 4.6000 so that the depreciation of ABE was

Less than as implied by parity as above?