Page 165 - Microsoft Word - 00 ACCA F1 Notes Prelims.docx

P. 165

Professional ethics in accounting and business

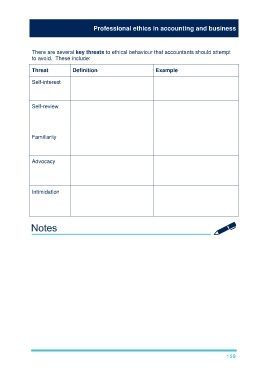

There are several key threats to ethical behaviour that accountants should attempt

to avoid. These include:

Threat Definition Example

Self-interest The auditor is reluctant to take Owning shares in a client

actions that are adverse to the

interests of the audit firm

Self-review The auditor is predisposed to Auditing financial statements that

accept/reluctant to question the have been prepared by the audit

work done by others in the audit firm

firm

Familiarity The auditor is predisposed to An audit team member has a

accept/reluctant to question the close family member working in

work done by the audit client the client accounts department

Advocacy The auditor takes Promoting the client’s shares in a

management’s side, adopting a share issue

position closely aligned with

management

Intimidation The auditor’s conduct is The client threatens the auditor

influenced by fear who is suggesting that a modified

opinion on the financial

statements will be given

159