Page 63 - Microsoft Word - 00 P1 IW Prelims.docx

P. 63

Non-current assets, agriculture and inventories

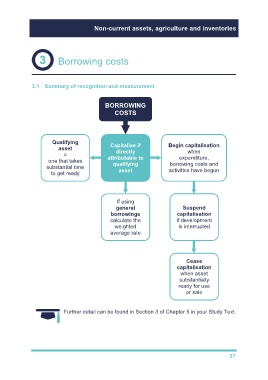

Borrowing costs

3.1 Summary of recognition and measurement

BORROWING

COSTS

Qualifying Capitalise if Begin capitalisation

asset directly when

=

one that takes attributable to expenditure,

borrowing costs and

substantial time qualifying activities have begun

to get ready asset

If using

general Suspend

borrowings capitalisation

calculate the if development

weighted is interrupted

average rate

Cease

capitalisation

when asset

substantially

ready for use

or sale

Further detail can be found in Section 3 of Chapter 5 in your Study Text.

57