Page 10 - FINAL CFA II SLIDES JUNE 2019 DAY 4

P. 10

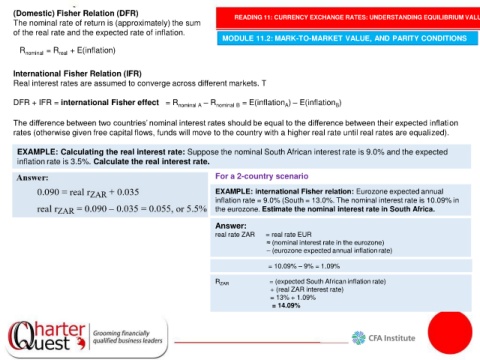

(Domestic) Fisher Relation (DFR) READING 11: CURRENCY EXCHANGE RATES: UNDERSTANDING EQUILIBRIUM VALUE

The nominal rate of return is (approximately) the sum

of the real rate and the expected rate of inflation.

MODULE 11.2: MARK-TO-MARKET VALUE, AND PARITY CONDITIONS

R nominal = R real + E(inflation)

International Fisher Relation (IFR)

Real interest rates are assumed to converge across different markets. T

DFR + IFR = international Fisher effect = R nominal A – R nominal B = E(inflation ) – E(inflation )

B

A

The difference between two countries’ nominal interest rates should be equal to the difference between their expected inflation

rates (otherwise given free capital flows, funds will move to the country with a higher real rate until real rates are equalized).

EXAMPLE: Calculating the real interest rate: Suppose the nominal South African interest rate is 9.0% and the expected

inflation rate is 3.5%. Calculate the real interest rate.

For a 2-country scenario

EXAMPLE: international Fisher relation: Eurozone expected annual

inflation rate = 9.0% (South = 13.0%. The nominal interest rate is 10.09% in

the eurozone. Estimate the nominal interest rate in South Africa.

Answer:

real rate ZAR = real rate EUR

≈ (nominal interest rate in the eurozone)

– (eurozone expected annual inflation rate)

= 10.09% – 9% = 1.09%

R ZAR = (expected South African inflation rate)

+ (real ZAR interest rate)

= 13% + 1.09%

= 14.09%