Page 4 - FINAL CFA II SLIDES JUNE 2019 DAY 4

P. 4

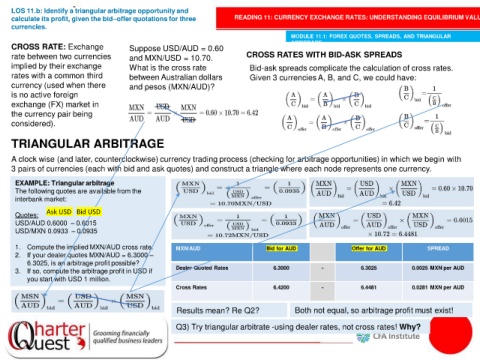

LOS 11.b: Identify a triangular arbitrage opportunity and

calculate its profit, given the bid–offer quotations for three READING 11: CURRENCY EXCHANGE RATES: UNDERSTANDING EQUILIBRIUM VALUE

currencies.

MODULE 11.1: FOREX QUOTES, SPREADS, AND TRIANGULAR

ARBITRAGE

CROSS RATE: Exchange Suppose USD/AUD = 0.60

rate between two currencies and MXN/USD = 10.70. CROSS RATES WITH BID-ASK SPREADS

implied by their exchange What is the cross rate Bid-ask spreads complicate the calculation of cross rates.

rates with a common third between Australian dollars Given 3 currencies A, B, and C, we could have:

currency (used when there and pesos (MXN/AUD)?

is no active foreign

exchange (FX) market in

the currency pair being

considered).

TRIANGULAR ARBITRAGE

A clock wise (and later, counterclockwise) currency trading process (checking for arbitrage opportunities) in which we begin with

3 pairs of currencies (each with bid and ask quotes) and construct a triangle where each node represents one currency.

EXAMPLE: Triangular arbitrage

The following quotes are available from the

interbank market:

Quotes: Ask USD Bid USD

USD/AUD 0.6000 – 0.6015

USD/MXN 0.0933 – 0.0935

1. Compute the implied MXN/AUD cross rate. MXN/AUD Bid for AUD Offer for AUD SPREAD

2. If your dealer quotes MXN/AUD = 6.3000 –

6.3025, is an arbitrage profit possible?

3. If so, compute the arbitrage profit in USD if Dealer Quoted Rates 6.3000 - 6.3025 0.0025 MXN per AUD

you start with USD 1 million.

Cross Rates 6.4200 - 6.4481 0.0281 MXN per AUD

Results mean? Re Q2? Both not equal, so arbitrage profit must exist!

Q3) Try triangular arbitrate -using dealer rates, not cross rates! Why?