Page 14 - Microsoft Word - 00 IWB ACCA F7.docx

P. 14

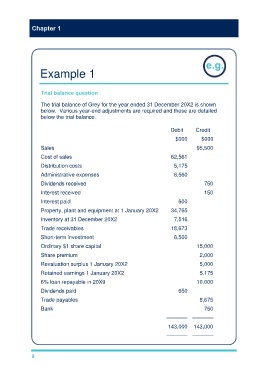

Chapter 1

Example 1

Trial balance question

The trial balance of Grey for the year ended 31 December 20X2 is shown

below. Various year-end adjustments are required and these are detailed

below the trial balance.

Debit Credit

$000 $000

Sales 95,500

Cost of sales 62,561

Distribution costs 5,175

Administrative expenses 6,560

Dividends received 750

Interest received 150

Interest paid 600

Property, plant and equipment at 1 January 20X2 34,765

Inventory at 31 December 20X2 7,516

Trade receivables 18,673

Short-term investment 6,500

Ordinary $1 share capital 15,000

Share premium 2,000

Revaluation surplus 1 January 20X2 5,000

Retained earnings 1 January 20X2 5,175

6% loan repayable in 20X9 10,000

Dividends paid 650

Trade payables 8,675

Bank 750

––––––– –––––––

143,000 143,000

––––––– –––––––

8