Page 238 - FR Integrated Workbook 2018-19

P. 238

Chapter 17

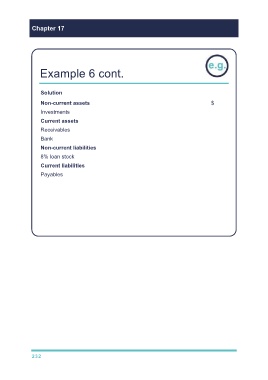

Example 6 cont.

Solution

Non-current assets $

3

4

Investments (8,000 – 3,500 – 300 ) 4,200

Current assets

2

1

Receivables (1,400 + 650 – 100 – 400 ) 1,550

1

Bank (600 + 150 + 100 ) 850

Non-current liabilities

4

8% loan stock (4,000 + 500 – 300 ) 4,200

Current liabilities

2

Payables (2,800 + 1,300 – 400 ) 3,700

1 Cash in transit, calculated as the difference between the payables and

receivables balances, $500 – $400 = $100.

2 Remove the balanced receivables and payables.

3 Remove the cost of investment, recorded in the goodwill calculation.

4 P’s investment in S’s loan stock is $500 × 60% = $300.

232