Page 336 - FR Integrated Workbook 2018-19

P. 336

Chapter 24

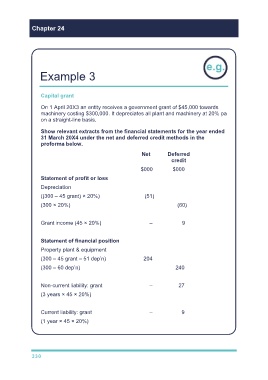

Example 3

Capital grant

On 1 April 20X3 an entity receives a government grant of $45,000 towards

machinery costing $300,000. It depreciates all plant and machinery at 20% pa

on a straight-line basis.

Show relevant extracts from the financial statements for the year ended

31 March 20X4 under the net and deferred credit methods in the

proforma below.

Net Deferred

credit

$000 $000

Statement of profit or loss

Depreciation

((300 – 45 grant) × 20%) (51)

(300 × 20%) (60)

Grant income (45 × 20%) – 9

Statement of financial position

Property plant & equipment

(300 – 45 grant – 51 dep’n) 204

(300 – 60 dep’n) 240

Non-current liability: grant – 27

(3 years × 45 × 20%)

Current liability: grant – 9

(1 year × 45 × 20%)

330