Page 28 - F6 Slide - VAT Part 4 - Lecture Day 5

P. 28

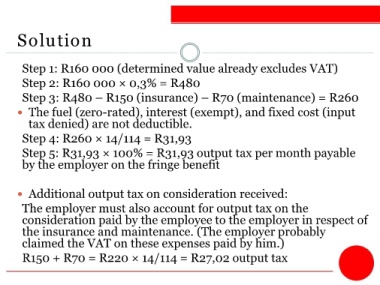

Solution

Step 1: R160 000 (determined value already excludes VAT)

Step 2: R160 000 × 0,3% = R480

Step 3: R480 – R150 (insurance) – R70 (maintenance) = R260

The fuel (zero-rated), interest (exempt), and fixed cost (input

tax denied) are not deductible.

Step 4: R260 × 14/114 = R31,93

Step 5: R31,93 × 100% = R31,93 output tax per month payable

by the employer on the fringe benefit

Additional output tax on consideration received:

The employer must also account for output tax on the

consideration paid by the employee to the employer in respect of

the insurance and maintenance. (The employer probably

claimed the VAT on these expenses paid by him.)

R150 + R70 = R220 × 14/114 = R27,02 output tax