Page 254 - F1 - AB Integrated Workbook STUDENT 2018-19

P. 254

Chapter 16

Internal auditing and external auditing

6.1 Differences between internal and external audit

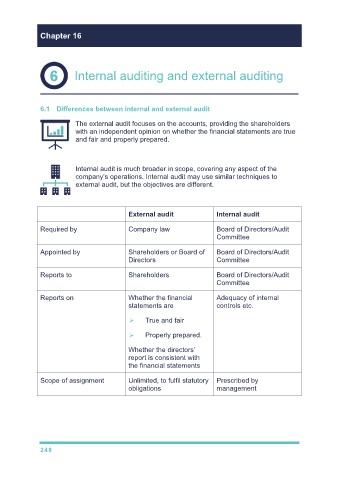

The external audit focuses on the accounts, providing the shareholders

with an independent opinion on whether the financial statements are true

and fair and properly prepared.

Internal audit is much broader in scope, covering any aspect of the

company’s operations. Internal audit may use similar techniques to

external audit, but the objectives are different.

External audit Internal audit

Required by Company law Board of Directors/Audit

Committee

Appointed by Shareholders or Board of Board of Directors/Audit

Directors Committee

Reports to Shareholders Board of Directors/Audit

Committee

Reports on Whether the financial Adequacy of internal

statements are controls etc.

True and fair

Properly prepared.

Whether the directors’

report is consistent with

the financial statements

Scope of assignment Unlimited, to fulfil statutory Prescribed by

obligations management

248