Page 372 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 372

Chapter 19

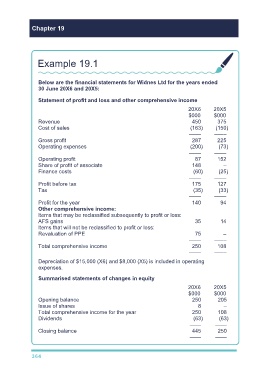

Example 19.1

Below are the financial statements for Widnes Ltd for the years ended

30 June 20X6 and 20X5:

Statement of profit and loss and other comprehensive income

20X6 20X5

$000 $000

Revenue 450 375

Cost of sales (163) (150)

–––– ––––

Gross profit 287 225

Operating expenses (200) (73)

–––– ––––

Operating profit 87 152

Share of profit of associate 148 –

Finance costs (60) (25)

–––– ––––

Profit before tax 175 127

Tax (35) (33)

–––– ––––

Profit for the year 140 94

Other comprehensive income:

Items that may be reclassified subsequently to profit or loss:

AFS gains 35 14

Items that will not be reclassified to profit or loss:

Revaluation of PPE 75 –

–––– ––––

Total comprehensive income 250 108

–––– ––––

Depreciation of $15,000 (X6) and $8,000 (X5) is included in operating

expenses.

Summarised statements of changes in equity

20X6 20X5

$000 $000

Opening balance 250 205

Issue of shares 8 –

Total comprehensive income for the year 250 108

Dividends (63) (63)

–—– —––

Closing balance 445 250

–—– –—–

364