Page 12 - PowerPoint Presentation

P. 12

Share-based Payment

Accounting For SBP

Introductory example:

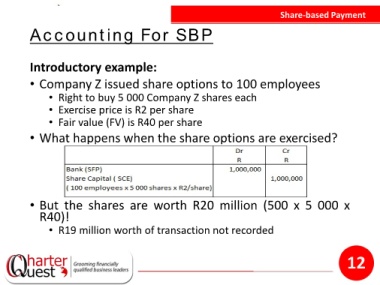

• Company Z issued share options to 100 employees

• Right to buy 5 000 Company Z shares each

• Exercise price is R2 per share

• Fair value (FV) is R40 per share

• What happens when the share options are exercised?

• But the shares are worth R20 million (500 x 5 000 x

R40)!

• R19 million worth of transaction not recorded

12