Page 101 - Microsoft Word - 00 - Prelims.docx

P. 101

Non-current assets: disposal and revaluation

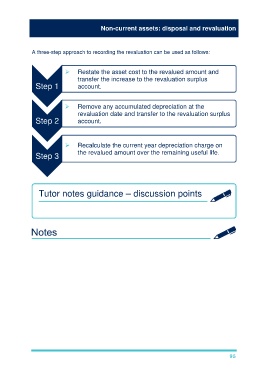

A three-step approach to recording the revaluation can be used as follows:

Restate the asset cost to the revalued amount and

transfer the increase to the revaluation surplus

Step 1 account.

Remove any accumulated depreciation at the

revaluation date and transfer to the revaluation surplus

Step 2 account.

Recalculate the current year depreciation charge on

Step 3 the revalued amount over the remaining useful life.

Tutor notes guidance – discussion points

Take students through Illustration 1 and 2 from Chapter 8 of the Study Text.

95