Page 159 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 159

Accounting for overheads

Production overhead account

The production overhead account gathers all of the production overheads (or indirect

costs) in a period.

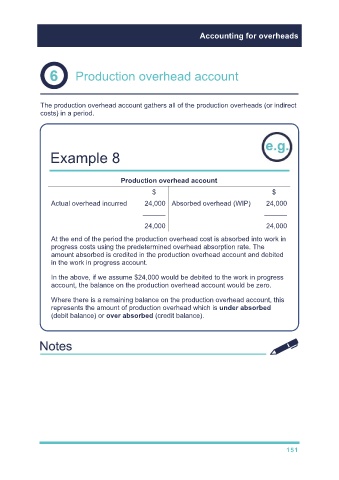

Example 8

Production overhead account

$ $

Actual overhead incurred 24,000 Absorbed overhead (WIP) 24,000

–––––– ––––––

24,000 24,000

At the end of the period the production overhead cost is absorbed into work in

progress costs using the predetermined overhead absorption rate. The

amount absorbed is credited in the production overhead account and debited

in the work in progress account.

In the above, if we assume $24,000 would be debited to the work in progress

account, the balance on the production overhead account would be zero.

Where there is a remaining balance on the production overhead account, this

represents the amount of production overhead which is under absorbed

(debit balance) or over absorbed (credit balance).

151