Page 229 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 229

Process costing

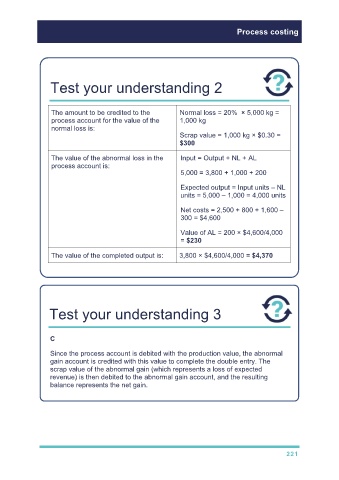

Test your understanding 2

The amount to be credited to the Normal loss = 20% × 5,000 kg =

process account for the value of the 1,000 kg

normal loss is:

Scrap value = 1,000 kg × $0.30 =

$300

The value of the abnormal loss in the Input = Output + NL + AL

process account is:

5,000 = 3,800 + 1,000 + 200

Expected output = Input units – NL

units = 5,000 – 1,000 = 4,000 units

Net costs = 2,500 + 800 + 1,600 –

300 = $4,600

Value of AL = 200 × $4,600/4,000

= $230

The value of the completed output is: 3,800 × $4,600/4,000 = $4,370

Test your understanding 3

C

Since the process account is debited with the production value, the abnormal

gain account is credited with this value to complete the double entry. The

scrap value of the abnormal gain (which represents a loss of expected

revenue) is then debited to the abnormal gain account, and the resulting

balance represents the net gain.

221