Page 372 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 372

Chapter 15

1.2 Standard cost card

Once standard costs for a product or service have been set, they are presented in a

standard cost card.

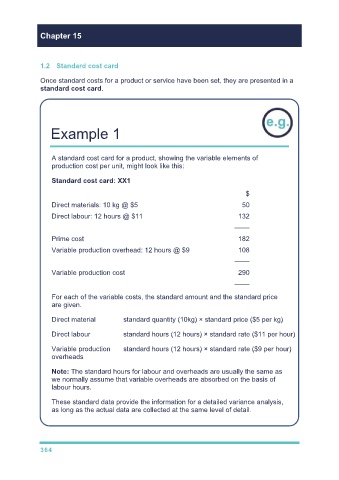

Example 1

A standard cost card for a product, showing the variable elements of

production cost per unit, might look like this:

Standard cost card: XX1

$

Direct materials: 10 kg @ $5 50

Direct labour: 12 hours @ $11 132

––––

Prime cost 182

Variable production overhead: 12 hours @ $9 108

––––

Variable production cost 290

––––

For each of the variable costs, the standard amount and the standard price

are given.

Direct material standard quantity (10kg) × standard price ($5 per kg)

Direct labour standard hours (12 hours) × standard rate ($11 per hour)

Variable production standard hours (12 hours) × standard rate ($9 per hour)

overheads

Note: The standard hours for labour and overheads are usually the same as

we normally assume that variable overheads are absorbed on the basis of

labour hours.

These standard data provide the information for a detailed variance analysis,

as long as the actual data are collected at the same level of detail.

364