Page 48 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 48

Chapter 4

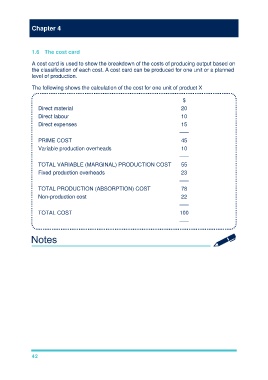

1.6 The cost card

A cost card is used to show the breakdown of the costs of producing output based on

the classification of each cost. A cost card can be produced for one unit or a planned

level of production.

The following shows the calculation of the cost for one unit of product X

$

Direct material 20

Direct labour 10

Direct expenses 15

–––

PRIME COST 45

Variable production overheads 10

–––

TOTAL VARIABLE (MARGINAL) PRODUCTION COST 55

Fixed production overheads 23

–––

TOTAL PRODUCTION (ABSORPTION) COST 78

Non-production cost 22

–––

TOTAL COST 100

–––

42